Building a generational business is hard - we do our best to help you get through the earliest stages of doing so, including through our content.

Focal. All rights reserved. © 2026

Designed by Casa Mkali.

I read Howard Marks’ memos religiously.

No one is better at explaining complex topics related to investing in the simple and clear way he does. And often, the lessons he shares in and around investing are applicable well beyond the world of generating financial returns too.

In his most recent memo “fewer losers or more winners”, Howard discusses the role of risk bearing.

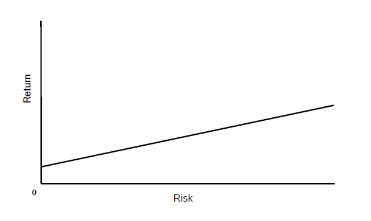

In school, like him, I was taught to view the relationship between risk and return as follows:

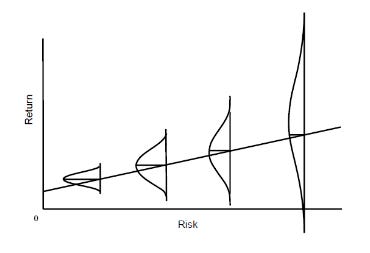

Howard argues regarding the risk / return framework:

The more I thought about it, the more unhappy I was with the way the linear presentation of the purported relationship tells investors that they can count on achieving higher returns as a result of taking more risk. After all, if that were really the case, risky investments wouldn’t be riskier. Thus, in my memo Risk (January 2006), I suggested a different way of depicting the relationship by superimposing on the line a series of bell-shaped probability distributions turned on their side:

Rather than implying that taking more risk – moving from left to right in the graph – assures higher returns, this new way of looking at the relationship suggests that as you take more risk, (a) the expected return increases, as per the original version above; (b) the range of possible outcomes becomes wider; and (c) the bad possibilities become worse. In other words, riskier investments introduce the potential for higher returns, but also the possibility of other less-desirable side effects. That’s why they’re described as being riskier.

This is a simple yet great way to think about taking risk both within investing as well as beyond, including company building.

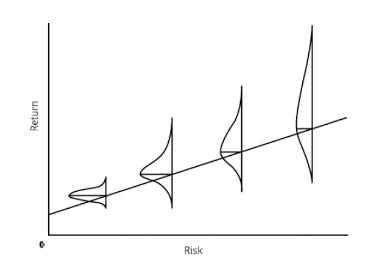

Within investing, the graph looks as following (from his memo):

Treasury bills / bonds sit on the low risk end of the spectrum while the world I live in - venture - sits on the risky end where some funds will return >10x while more than half the funds raised return <1x. Making manager selection, portfolio construction, etc even more important.

In company building, the framework from above regarding risk / return and distribution of outcomes is applicable to most high impact decisions you’re making. This includes the very important decision re how to best finance your business / growth:

This simple yet powerful framework is a good one to think through again the next time you have an impactful decision to make.

To add to the framework - towards the end of the memo, Howard also talks about “alpha” (i.e. individual investing skill).

Investors who possess alpha have the ability to alter the shape of the distributions in the graphs above so that they’re not symmetrical, in that the portion of the distribution representing the less desirable outcomes is smaller than the portion representing the better ones. In fact, that’s what alpha really means: Investors with alpha can go into a market and, by applying their skill, access the upside potential offered in that market without taking on all the downside risk. […] the key characteristic of superior investing is asymmetry – having more upside than downside. Alpha enables exceptional investors to modify the probability distributions such that they are biased toward the positive, resulting in superior risk-adjusted returns.

If alpha is the ability to earn return without taking fully commensurate risk, investors possessing it can do so by either reducing risk while giving up less return or by increasing potential return with a less-than-commensurate increase in risk. […] Almost no investors possess both forms of alpha, and most possess neither. Investors who lack alpha shouldn’t expect to be able to produce either version of asymmetry – that is, to be able to generate superior risk-adjusted returns. However, most believe they do have it.

Harsh words. Yet, historical returns across asset classes confirm that most investors don’t possess alpha (i.e. don’t consistently outperform vs expected returns).

It’s something we think about a lot at focal - how do we create alpha / consistently outperform as a pre-seed VC firm in a venture market that is as crowded as it is / in an asset class that has such a wide distribution of outcomes? We believe we have an answer, are leaning into it as a firm and are betting the next decades of our professional lives on it. Whether we’re right, we’ll find out in a few years from now.

Like the risk / return framework, the concept of alpha doesn’t just apply to the world of investing but also business building.

Figuring out where you have an unfair / asymmetric advantage to have more upside than downside vs the rest of the market very much matters in the startup world too.

Founder domain expertise, a unique (non-obvious) insight, a significant strength in a skill essential to the business you’re building are amongst the things that can positively change the probability distribution of outcomes. Thus, we spend a lot of time looking for such “alpha” when we diligence pre-seed startups. And so should you as a startup founder / operator when thinking about what to build your company around / double down on. After all, you can only do one / very few things well at once with limited resource.

It’s hard / rare to find such an unfair / asymmetric advantage and more often than not, we get it wrong. But when we get it right, it can be life changing for both the founders we back as well as for us.

If you haven’t done so already, I can highly recommend signing up to Oaktree’s / Howard Marks’ insights.

Pascal